Home Renovation Loan - Truths

Table of ContentsThe Facts About Home Renovation Loan RevealedThe Only Guide to Home Renovation Loan7 Easy Facts About Home Renovation Loan ExplainedHome Renovation Loan Fundamentals ExplainedThe smart Trick of Home Renovation Loan That Nobody is Talking About

Think about a home improvement loan if you desire to refurbish your residence and offer it a fresh appearance. With the assistance of these fundings, you may make your home more aesthetically pleasing and comfortable to live in.There are lots of funding choices available to aid with your home remodelling. The best one for you will certainly depend upon just how much you require to borrow and just how rapidly you intend to pay it off. Brent Differ, Branch Manager at Assiniboine Lending institution, offers some sensible guidance. "The first point you ought to do is obtain quotes from several specialists, so you know the reasonable market price of the job you're obtaining done.

The main advantages of making use of a HELOC for a home remodelling is the versatility and reduced rates (commonly 1% above the prime rate). Additionally, you will just pay interest on the amount you take out, making this an excellent option if you require to pay for your home improvements in stages.

The primary negative aspect of a HELOC is that there is no fixed settlement timetable. You have to pay a minimum of the interest each month and this will certainly increase if prime rates go up." This is a great funding alternative for home remodellings if you intend to make smaller sized month-to-month settlements.

Home Renovation Loan Fundamentals Explained

Given the potentially long amortization period, you can finish up paying significantly even more interest with a mortgage refinance compared with other funding alternatives, and the prices connected with a HELOC will also use. home renovation loan. A home mortgage re-finance is successfully a brand-new home loan, and the rate of interest might be more than your current one

Prices and set-up costs are normally the like would certainly spend for a HELOC and you can settle the funding early without any penalty. Several of our clients will begin their improvements with a HELOC and afterwards switch to a home equity car loan once all the prices are validated." This can be a good home renovation funding choice for medium-sized projects.

Individual funding prices are commonly more than with HELOCs generally, prime plus 3%. And they usually have shorter-term durations of 5 years or less, which suggests higher settlement amounts." With charge card, the main disadvantage is the rate of interest can normally range in between 12% to 20%, so you'll want to pay the equilibrium off rapidly.

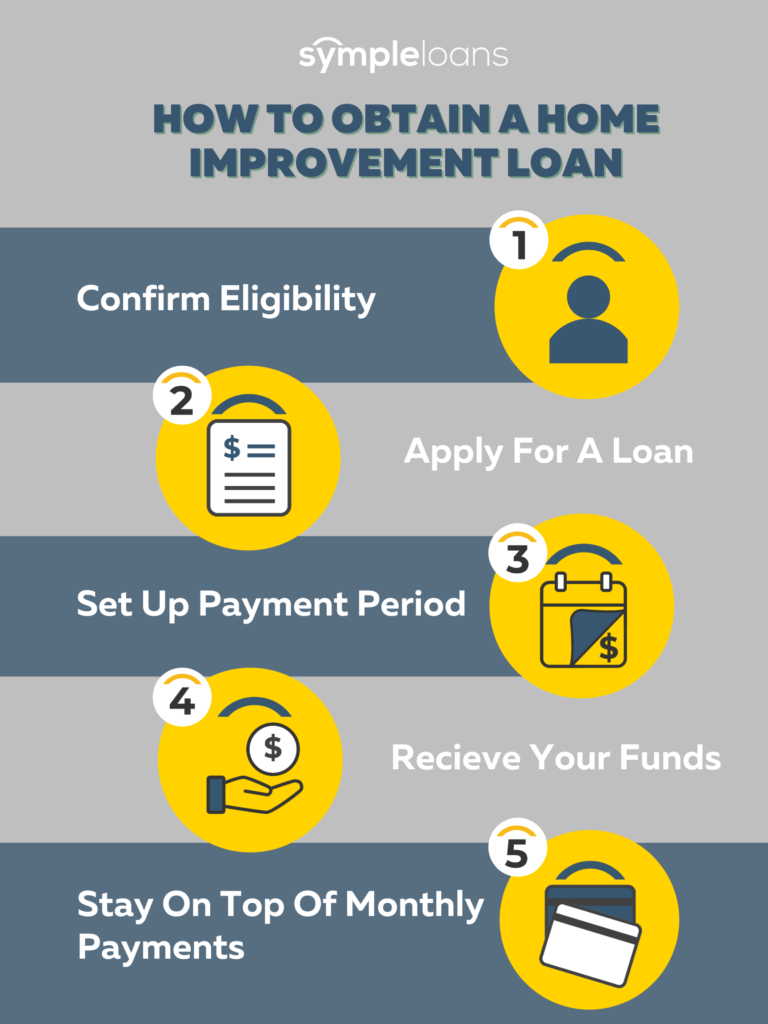

Home remodelling car loans are the funding alternative that allows property owners to remodel their homes without needing to dip right into their savings or splurge on high-interest credit report cards. There are a selection of home renovation funding resources readily available to choose from: Home Equity Line of Credit Scores (HELOC) Home Equity Finance Mortgage Refinance Personal Lending Credit Score Card Each of these funding alternatives features distinctive needs, like credit rating, owner's income, credit score restriction, and rates of interest.

The Basic Principles Of Home Renovation Loan

Before you take the plunge of making your desire home, you probably would like to know the a number of great post to read types of home renovation loans readily available in Canada. Below are some of the most common sorts of home restoration fundings each with its own collection of qualities and benefits. It is a kind of home enhancement lending that permits house owners to borrow a plentiful sum of cash at a low-interest rate.

These are helpful for massive improvement jobs and have reduced rates of interest than other sorts of individual fundings. A HELOC Home Equity Line of Credit is similar to a home equity lending that utilizes the worth of your home as safety and security. It operates as a charge card, where you can borrow according to your demands to fund your home restoration projects.

To be qualified, you must possess either a minimum of at the very least 20% home equity or if you have a home mortgage of 35% home equity for a standalone HELOC. Refinancing your home loan procedure involves replacing your present home mortgage with a brand-new one at a lower rate. It minimizes your monthly settlements and decreases the quantity of rate of interest you pay over your life time.

The Facts About Home Renovation Loan Uncovered

For this, you might need to provide a clear building strategy and budget for the renovation, consisting of determining the cost for all the products needed. Additionally, individual finances can be protected or unsecured with much shorter payback durations (under 60 months) and come with a greater rates of interest, depending upon your credit rating and revenue.

Some Ideas on Home Renovation Loan You Should Know

Store financing programs, i.e. Store credit history cards are offered by many home improvement stores in Canada, such as Home Depot or Lowe's. If you're preparing for small-scale home browse around this site enhancement or DIY projects, such as setting up new windows or restroom improvement, obtaining a store card through the merchant can be a very easy and fast process.